Table of Contents

- Defining Momentum Terminology in Academic Research

- Why Does Momentum Work?

- Momentum and Dynamic Asset Allocation

- The Story of How Momentum Became Accepted by the High Priest of Finance

- A Review of the Academic Momentum Research

- Conclusion

“If you rank stocks based on their past six months of returns, then returns over the next few months tend to go in the same direction at the extremes – extreme losers continue to lose and extreme winners continue to win. There’s a lot of speculation about why that happens……..But in my view that’s the biggest challenge to market efficiency.”

“Momentum is the premier anomaly”

Introduction

The investment industry is built on the assumption of a “goldilocks” utopian world where the market makes an 8% return every year without fail. Many financial planners implicitly believe that the markets will conform to accommodate investors’ time horizons. The flaw of averages is that any particular sample can vary widely from expectations. This can have catastrophic consequences for an investor’s ability to accumulate the needed funds to retire or ensure those funds last throughout their retirement. There are several reasons why we might expect the next decade to deviate from the past:

- The economy today is heavily dependent on fiscal and monetary policy.

- Stock valuations are very high by historical standards (Shiller).

- Interest rates are close to zero across most developed countries around the world.

- The banking system still remains wounded after being on the verge of collapse during the credit crisis in 2008.

- Global political tensions with Russia and China are becoming increasingly strained

While we cannot forecast what will happen, it is reasonable to say that the future could prove to be volatile and disappointing for investors. Navigating unknown waters requires adapting to changing conditions rather than charting a fixed course. This choice is analogous to the decision to have a dynamic or tactical portfolio versus a strategic (or static) allocation portfolio. Adaptation is the key to our approach, and we believe it is the key to investment survival in the real world. Being out of touch with the current trends exposes us to the dangers that exist in the present. A natural means of adaptation is to pay attention to what is actually happening and reward the asset classes that are positive while avoiding the asset classes that are negative. This is analogous to “going with the flow”, or following the course of momentum. Our Dynamic Asset Allocation Model primarily relies on momentum to make allocation decisions in order to be adaptive to changing market conditions. Using momentum within a dynamic asset allocation approach can enhance returns and reduce risk relative to a strategic portfolio approach.

Why do we think momentum is essential for portfolio management? The case is quite convincing as we will demonstrate in this paper:

- Momentum has been endorsed as the strongest and most robust factor in financial markets by top academics – many of whom are traditionally skeptical of active management.

- Momentum strategies have been used effectively by some of the best money managers in the world.

- Research has shown that momentum has been a durable strategy for over hundreds of years of market history.

- Most importantly, a momentum approach can be easily quantified into an objective set of rules that can be easily applied to any investment universe.

So why do we oppose the traditional approach of having portfolio managers and investment committees use their expert judgment to set asset allocation? The answer is simple; human decision-making has been shown in the research to be both biased and unreliable (Thaler, 1992). For example, classic studies by Tetlock (2005) used experts across various fields to make predictions about the future and demonstrated that they were only slightly better than chance. What is more interesting is that simple computer algorithms that used momentum rules1 significantly outperformed the experts. Consistent with Tetlock’s findings, academic research in finance has found that there are no fundamental or economic forecasting methods that have proven to be nearly as effective as momentum.

It is traditional for financial marketing materials to use a table of annual performance across sectors or asset classes to give investors a sense of historical perspective. Primarily this is done in an attempt to demonstrate to investors that there is no pattern in past performance, and hence the future is unpredictable. This observation is used as a justification for holding a passive diversified portfolio. An example of these annual performance tables is shown in the graphic below using broad asset classes:

As you can see in the Figure 1, there is no obvious pattern from year to year in asset class performance. This is consistent with arguments that asset class performance is unpredictable – but only from year to year. So where is the momentum effect? As it turns out we are looking at the wrong time scale. The momentum effect is a shorter-term phenomenon, and to see it in action we need to look more closely.

The basis of the momentum effect is that the past predicts the future whether we are looking at relative or absolute asset class performance. To implement a momentum strategy you need to choose a formation and a holding period. The formation period is the length of time you use to compute historical performance, while the holding period is defined as the length of time that you would hold a particular asset before rebalancing. The momentum effect exists with formation and holding periods that are between 1 to 12 months. Longer formation periods of 3 to 12 months used in tandem with holding periods of 1 to 6 months tend to be the most profitable (Jegadeesh and Titman, 1993). If an asset’s return is high relative to other assets on the basis of past performance, it tends to have good performance in the future. If an asset’s return is low relative to other assets it tends to have poor performance in the future. Furthermore, the sign of returns over the past 1 to 12 months tends to predict future performance over the next 1 to 12 months (Moskowitz,2012): positive past performance tends to be followed by positive future performance, while negative past performance is followed by negative future performance. Both momentum effects that we have highlighted tend to predict performance at shorter time frames than 12 months. As a consequence to be able to see the patterns we need to use a shorter time frame than annual performance. In the Figure 2 we zoom in to see the performance month to month instead of year to year using 2013 as an example.

As you can see the trends in asset class performance are much clearer than before. In fact they are remarkably predictable by comparison. Investors may recall that 2013 was terrible for bonds and commodities. Could one have avoided holding these losers by using momentum? On closer inspection the poor performance of both bonds and commodities seemed to be predictable; both asset classes hovered near the bottom of the rankings persistently the entire year. Furthermore, both bonds and commodities had negative returns as well for most of the year. Conversely, equities had a fantastic year and stocks (domestic), value, small cap and growth stocks were all top performers with consistently positive returns through 2013. A typical 60/40 investor would have still done well in 2013, but the 40% of their portfolio in bonds would have been a significant drag on performance. By observing these trends, they could have increased their equity allocation and achieved superior performance.

If we were to generate historical performance tables for other years few would have been as orderly as 2013. However, as we shall see this momentum effect is a consistent phenomenon throughout market history. Here are the results that show the performance of applying momentum as a trading strategy on a walk-forward basis (no hindsight) using the same asset classes in the previous table. In other words, each month we select a subset of the top (or bottom) performers using their past return and then hold them for the next month. We repeat this process every month over the historical time window and record the results of each portfolio computing the annualized return, risk and maximum drawdown in Figure 3:

There are a few observations to note. First, momentum rankings were strongly linked to future returns – winners had the best performance, while losers had the worst performance. Furthermore, the rankings were also strongly linked to risk metrics such as reward to risk (Sharpe ratio) or maximum drawdown. Low rankings especially led to consistently higher risk metrics, while higher rankings led to generally lower risk metrics. The top quintile (or top 3 of the 15 asset classes in Figure 3) using momentum rankings earns a 14.3% return – which substantially outperforms both an equal weight portfolio of all assets and also the S&P500 over time. Using an equal weight portfolio of stocks and bonds as a simple proxy for a balanced portfolio we find that the top quintile earns over 6% more per year on average with a similar level of risk and maximum drawdown. The bottom quintile of asset classes earns a paltry 1.5% annualized with higher risk metrics than all other portfolios. Clearly using momentum is an effective strategy for identifying both the winners and losers.

As we pointed out, the sign of past returns for Commodities and Bonds was consistently negative all through 2013. Does the sign of past returns also provide useful information? As it turns out the sign of past returns (whether the return is positive or negative) is an excellent indicator of whether an asset will go up or down. If that is the case then we should expect that using the sign of momentum should help reduce the risk of large drawdowns and possibly increase the return to holding a particular asset versus buy and hold. Using the same asset classes, we used momentum to hold a long position if the sign was positive and held t-bills if the sign was negative. Here are the results broken down for each asset individually in Figure 4:

For every single asset the reward to risk ratio was superior to buying and holding the underlying asset, and the drawdown was either the same or significantly lower. In most cases you actually improved the return versus buy and hold by looking at whether historical returns were positive or negative to determine whether or not to take a position in the underlying asset. This means that we have two different types of momentum that we can use to make investment decisions: the sign of past returns and the relative rank of returns. These results for both momentum rankings and using the sign of past returns have been validated in the academic research, and are essentially the exact same concepts that are referred to in the current literature. They simply carry different names.

Defining Momentum Terminology in Academic Research

There are two types of Momentum:

- Cross-Sectional Momentum (or relative strength/momentum) Assets are ranked on the basis of historical performance to predict the best future performing assets. In the chart below (Figure 5) we see three different assets (A, B and C) and their respective total returns. In this case, a momentum or cross-sectional momentum strategy would favor Asset A above B and C. In other words, Asset A is expected to outperform the other two assets. Asset B is expected to be the worst performing asset while C is expected to fall in the middle. In the academic research the traditional tests would hold a long position in Asset A (the “winner”) and a short position in Asset B (the “loser”). The performance of this portfolio would be called the excess return.

Figure 5: Cross-Sectional Momentum

Source: BSAM

Source: BSAM - Time Series Momentum (or absolute momentum/trend-following) – Time series momentum is used to determine whether one should hold a long (direction is predicted to be positive) or short position (direction is predicted to be negative) in a particular market. Time series or absolute momentum uses the relative total return of an asset to the risk-free rate/t-bills to determine whether returns are expected to be positive or negative. In the chart below, Asset A has positive time series/absolute momentum since its total return is greater than the return for t-bills. This means that Asset A is expected to have a positive excess return and one should hold a long position. In contrast Asset B has negative time series/absolute momentum since its total return is less than the return for t-bills.

Figure 6: Time Series Momentum

Source: BSAM

Source: BSAM

Therefore one should hold either a cash or short position in Asset B. In trend-following, it is common practice to compare the level of price (or cumulative total return series) in relation to the average price to predict whether an asset will have positive or negative performance. In the chart below (Figure 7) using the same underlying assets, we see that Asset A is above its moving average and therefore a long position is dictated. This is the same position dictated by time series/absolute momentum and they tend to hold identical positions most of the time. In contrast, Asset B is below its moving average and therefore a short or cash position would be dictated.

In general momentum/cross-sectional momentum is used to determine our relative preference for different assets but it does not tell us whether they are expected to have a positive or negative performance. For example, the most stocks in 2008 would have had negative performance. In contrast, time series/absolute momentum and trend-following are used to determine whether a long/short or cash position are dictated. By using both momentum methods it is possible to both enhance returns and reduce risk. It sets the basis for expectations for performance for different asset classes.

Why Does Momentum Work?

No one knows exactly why momentum works, but we believe that the explanation articulated by legendary hedge fund manager John Henry best describes why this approach is useful. Henry’s philosophy is based on the premise that market prices, rather than market fundamentals, are the key aggregation of information needed to make investment decisions. He explains that markets reflect people’s expectations, and the changes in these expectations manifest themselves as price trends.

No one consistently can predict anything, especially investors. Prices, not investors, predict the future. Despite this, investors hope or believe that they can predict the future, or someone else can. A lot of them look to you to predict what the next macroeconomic cycle will be. We rely on the fact that other investors are convinced that they can predict the future, and I believe that’s where our profits come from. I believe it’s that simple…

We live in an uncertain world. One cannot predict the future of anything. In an uncertain world, identifying and following trends may be the only reasonable investment approach over the long term.

John Henry, (Source: Turtle Trader)

It is important to point out that John Henry is a “trend-follower” (a subset of the two types of momentum) and has one of the best track records of performance of any other investor. Real world performance is perhaps the best endorsement of the viability of any style or type of investment approach. Academic research is useful, but the real litmus test is whether a concept can be applied to make money net of transaction costs and fees instead of looking in the rear view mirror. Before we review the academic support for momentum and its close cousin “trend-following,” let’s take a look at the best performing investment managers with a long track record (over 20 years) and see if there is a common style that they share.

In our first paper, Dynamic Asset Allocation: Foundations, we showed evidence that the market is macro-inefficient; the majority of active management decisions should focus on broad asset allocation. In support of this contention, we find that over the past 20 years an incredible 10 out of 11 of the best investment managers in the world follow a “macro” approach. Warren Buffett remains the exception as being the only investor on the list that uses a bottom-up or security selection approach. More importantly, 6 out of 11 managers, and the ones with the best results, employ a quantitative trend-following approach across a broad set of global markets – which share the same underlying principles as our approach to Dynamic Asset Allocation.

Momentum and Dynamic Asset Allocation

Here is a summary of the evidence we have seen so far:

- Momentum can help to predict relative performance; asset classes with the highest returns are likely to outperform and asset classes with the lowest returns are likely to underperform;

- The sign of past returns or the sign of momentum can help predict whether an asset is likely to go up or down. This can help improve returns, but more importantly it consistently reduces the risk of holding a particular asset. This phenomena is consistent across major asset classes;

- 90% of the best money managers with the highest returns and longest track records focus on a macro approach using broad asset classes (and other markets like currencies) regardless of whether they use discretionary judgment or quantitative rules;

- Most of the best money managers use momentum.

This evidence should lead investors to question the wisdom of traditional portfolio management:

- Why should I hold a strategic (passively invested) portfolio (like 60/40) if I can dynamically shift to stay in tune with market trends?

- Why should we bother using human judgment to make forecasts when we can use simple models that have proven to be more effective?

- How can risk be effectively managed by making long-term assumptions?

The answers are obvious, if you accept that momentum “works” then by extension it is a necessary and critical component in portfolio management to enhance returns and manage risk. This concept is critical to our Dynamic Asset Allocation approach. As momentum changes across assets and for each individual asset, the portfolio dynamically changes to respond. This may not seem intellectual enough to be satisfying to many discretionary portfolio managers. These same individuals often attempt to invalidate a momentum approach on the grounds that it doesn’t capture all of the variables that they are likely to analyze. But there is no way of knowing whether a particular discretionary manager (no matter how eloquent or what their pedigree is) is likely to demonstrate superior performance. In contrast, the simple application of momentum in its purest form has produced world-class money managers. While the momentum phenomenon is often dismissed, it is important to remember that Tetlock demonstrated it is hard to beat as a universal decision-making tool.

The Story of How Momentum Became Accepted by the High Priest of Finance

The research supporting the application of momentum to investing strategies is both vast and interesting. The evolution of thought towards a momentum approach was met initially with controversy from the camp of academia and also passive investors. To place the research into proper context it is important to also recount the story and the characters behind momentum investing. This story also demonstrates why advisors and investors should be wary of blindly accepting theoretical claims from academia. In the world of academia, professors are slow to change their mind and will vigorously defend their early theories to save face. This is true of many industries, but unlike the world of academia, in the investment world you are held accountable for your performance rather than your consistency in thinking. As a result, you need to have an open mind and seek to find the middle ground. In this story, we document how one professor reshaped both academic finance and the world of investment products yet managed to take the rare step of changing his minds to accept new information. A comprehensive look at the history of the momentum research and its application in the real world has supported a consensus that momentum is a timeless and effective strategy.

The High Priest of Academic Finance

Eugene Fama is considered to be the “high priest” of academic finance. His dissertation, “The Behavior of Stock Market Prices,” along with his article “Efficient Capital Markets: A Review of Theory and Empirical Work,” published in the Journal of Finance in 1970, presented a revolutionary new approach to understanding how financial markets operate. His work went on to provide the intellectual foundation for passively-managed and indexed mutual funds. This became a very popular new approach to investing in the 70’s and has since become the basis for strategic allocation. Fama is a professor of finance at the famed University of Chicago and sits on the board of Dimensional Fund Advisors (DFA) which manages over $381 billion for investors worldwide, with 11 offices around the globe. Dimensional Fund Advisors (DFA) was founded on Fama’s principles and continues to be shaped by his work.

Fama’s early philosophy was that active management provides no additional value. Purchasing a basket of stocks that reflects the broader stock market should yield better results than individual stock selection. Eugene Fama is also known as the father of the efficient markets hypothesis (EMH). The EMH broadly implies that:

- Markets are efficient and reflect all known information;

- Markets are not predictable;

- Human beings are rational and this drives market efficiency; and

- Investors are better off with a passive approach.

In 1993, the largely theoretical foundation that the EMH was founded on was replaced by a more empirical approach. Fama and finance professor Ken French created the “Fama-French Three-Factor Model” which was meant to replace William Sharpe’s Capital Asset Pricing Model (CAPM) which stipulates that the return you earned on a given asset is directly proportional to its systematic risk or volatility. The CAPM (and by extension the EMH) had come under severe attack for its lack of empirical support for explaining stock returns in the real world. The three-factor model was an attempt to restore order and respectability to proponents of the EMH. This model asserted that stock returns are primarily due to three factors: market risk, size risk and value risk. The three-factor model became widely adopted as a benchmark for testing new factors to determine if they added any marginal value for explaining stock returns. Curiously, no economic or theoretical explanation was offered for why value and size should be added to the model. This was unusual since Fama was notorious for relying on theoretical arguments to invalidate the empirical results of other authors. Apparently the fact that empirically the three-factor model produced a better statistical fit than the CAPM was enough validation.

The Historic Study on Momentum

Ironically during the same year, Jegadeesh and Titman (1993) published their famous paper: “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.” The authors posed a critical argument: “If stock prices either overreact or underreact to information, then profitable trading strategies that select stocks based on their past returns will exist.” In other words if human beings are not completely rational and make decisions based upon emotion, then momentum strategies should prove to be effective. Supporting their premise, they found that strategies that buy past winners and sell past losers based on historical returns deliver significant abnormal returns over the 1965 to 1989 period of as much as 12% per year on average. This research spurred the growth of supporting studies on momentum investing and was one of the key findings that drove interest in “behavioural finance” – or the study of how humans make financial decisions.

The Student: Applying Momentum in the Real World

A lot of what we do, a fair amount original at our firm, a lot of it taken from academia, is to say, “Can we make clients real money with this stuff?

I started my career in 1990 so I’m on 24 years of an out-of-sample test.

Cliff Asness, Founder & CIO of AQR

Around the same time, Cliff Asness, a doctoral student and teaching assistant of Eugene Fama, published his PhD dissertation: “Variables that Explain Stock Returns”(1994). The paper highlighted momentum as a key factor explaining stock returns and a significant source of profits. He also found that value was a strong and complementary factor – but this was already accepted by Fama in his three-factor model. By his own admission, Asness was actually frightened to present the findings to Fama for fear of being ridiculed. Fama told him that if it was “in the data” then he should feel comfortable with his findings (source: The Quants). In a separate interview, Asness claimed that the only reason Fama let him graduate was that he recommended pairing momentum with value (which was already considered acceptable). The next year, Asness went to Goldman Sachs and founded “Global Alpha” which became world famous as one of the earliest and most successful quantitative hedge funds. In 1998, Asness left Goldman Sachs to found AQR (Applied Quantitative Research) which manages approximately $122.2 billion in AUM with offices worldwide. AQR is an alternative asset management firm that has had spectacular success; currently it is one of the largest and most successful hedge fund managers worldwide, and has recently branched out into mutual funds. In terms of historical performance, over past 16 years the Absolute Return strategy produced annual returns of 10.8% after fees (typically 2% management fee and 20% performance fee), including the results of Global Alpha from the three years Asness ran it using the same approach. That compares with 6.8% for the S&P 500 (SPX). (Source: Fortune).

The High Priest Recants

After nearly 20 years of “out-of-sample” performance and plenty of real-world validation by various asset managers like AQR, Fama decided to publish a “Four-Factor Model” in 2011, the newly added 4th factor being momentum. Apparently, the original Fama-French three-factor model didn’t account for enough variation in stock prices, and adding momentum seemed to improve results. The addition of momentum to the model again was not explained using any theoretical basis, much like the addition of value and size to the CAPM in 1993. It seemed as if Fama and French simply had to acknowledge the weight of historical and real world evidence in order to avoid sounding biased.

Since the empirical performance of momentum was equally if not more compelling to value and size at the time of the publication of the three-factor model, one has to wonder if some sort of personal bias prevented Fama from using it in the first place. In fact, Asness has openly stated as much when discussing why he was afraid of talking about momentum with Fama: “Because it’s a perfect Chicago dissertation to say, “Look, these crazy people on Wall Street use price momentum. Doesn’t work at all. They’re wasting their money.”(Source: Forbes Interview, 2014) The fact that it took Fama nearly 20 years to acknowledge the existence of momentum with no other explanation other than the data itself shows that he probably inherently disliked the fact that ordinary practitioners were using it.

Fama’s bias towards the momentum effect proves that it can be risky to put faith in the objectivity of theoretical claims or skeptical remarks made by academics. They are often far less open-minded than practitioners to new ideas, and are perhaps less willing or incentivized (due to fear of being rejected for publication) to acknowledge that they are wrong until long after the fact. Interestingly enough, Fama also seems to have recently put his money where his mouth is: DFA has long incorporated the insights from the factor models introduced by Fama’s research, and curiously it was revealed that momentum is in fact currently considered within their trading models (source: Morningstar).

A Review of the Academic Momentum Research

To briefly recap terminology, the academic and practitioner research currently identifies two types of momentum: 1) cross-sectional momentum: the best performing assets by historical return tend to outperform the worst performing assets. This is often used interchangeably with “relative-strength” investing. 2) time series momentum: an asset’s own past returns predict its future return, specifically the sign of past returns tends to be the most useful for predicting the direction of future performance. This is also used interchangeably with “trend-following” or what many others call “absolute momentum”. Cross-sectional momentum is a strategy that is used to identify the best performing assets, while time series momentum is used to identify whether the expected future direction of an asset is likely to be up or down. Both strategies are complementary as cross-sectional momentum can increase returns (and reduce risk if used with broad asset classes versus just within an asset class like individual stocks), while time series momentum is primarily useful for controlling risk and increasing the consistency of returns (although it can also enhance returns).

Momentum Within Asset Classes

The original studies on cross-sectional momentum were introduced by Jegadeesh and Titman in 1993. The data used was based on the post WW2 era. Their historic study focused on the application of cross-sectional momentum to selecting individual stocks. In other words, their study demonstrated momentum within the equity asset class (US Stocks in this case). Asness et al. confirm their findings over a longer 86 year period between 1927 and 2013. They found that the spread of recent winners over recent losers in individual stocks averaged 8.3% a year. The following chart, Figure 9, is adapted from the Fama and French Library showing the linear separation between different momentum decile portfolios of US stocks.

To further prove the durability and timelessness of cross-sectional momentum strategies on US stocks, Geczy and Samonov appropriately called their 2012 study “212 Years of Price Momentum: The World’s Longest Backtest: 1801-2012”. A graph taken from their paper shows the remarkable divergence between the performance of past winners versus past losing stocks using historical returns:

The data is extremely compelling for the application of cross-sectional momentum to individual stocks. However, analysis and visual observation shows that there have been multiple periods where momentum has not worked: i.e. the losing stocks outperformed or matched the performance of the winning stocks. This is an important observation and shows that some of the best strategies are durable mainly because they do not work all the time! After all, the reason momentum exists is partly because of investor over and under-reaction in the first place. Geczy and Samonov show that a large part of the driver in the consistency of momentum profits is actually the state of the equity market itself: in bull markets, the winners reliably outperform the losers. Legendary investor William O’Neil of Investor’s Business Daily, who has made a fortune through momentum investing, has long advocated that investors should avoid a momentum approach in bear markets. Consistent with this advice, the data shows that in bear markets, cross-sectional momentum has virtually no edge.

The performance in bull markets is very consistent with most of the returns coming from the long side versus the short side. However, as the bull market length grows, the systematic risk of a cross-section stock momentum strategy grows.

In bear markets, cross-sectional momentum shows a much smaller edge that is driven more by shorting losing stocks than buying winning stocks. This makes sense since the average stock performance is likely to be negative in a down market. However, as the duration of the bear market increases, the edge to cross-sectional momentum becomes highly volatile.

In general, the Geczy/Samonov study demonstrates that momentum is not a fad, but rather a historical phenomena that has survived multiple generations across different economic regimes. If the traditional recommendation that buying and holding stocks should provide a long-term return is based on looking at over a hundred years of market history, the empirical evidence is perhaps just as compelling that one should earn superior returns to buying winning stocks and avoiding losing stocks.

The durability of cross-sectional momentum seems universal and applicable to other asset classes than individual stocks. In a good summary by Asness, Frazzini, Israel, and Moskowitz (2014): Fact, Fiction, and Momentum Investing, the authors note that cross-sectional momentum “works” and is validated in many other studies covering 40 different countries and more than a dozen other asset classes (such as bonds, currencies, commodities). For example, Miffre and Rallis (2007) conducted a 26-year study on 31 different commodities contracts using a standard momentum methodology. They found that the top quintile of commodities outperformed the bottom quintile by nearly 10% annually. Derwall et al. (2008) shows a pronounced momentum effect in real estate via REITs (real estate investment trusts). To capture these effects, we employ a “real asset” category that includes inflation-sensitive instruments such as commodity ETFs and REIT ETFs.

Menkoff (2012) conducted a study with 48 different currencies between 1976 and 2010 using conventional momentum strategies and found that the “winner” currencies with the best past performance outperformed the “loser” currencies with the worst performance by nearly 10% annually. However the best performers were concentrated in illiquid and smaller currencies. Furthermore the overall volatility of currencies tend to be low as well as profitability on the long side. While the findings of the study support the broad robustness of the cross-sectional momentum effect, we chose to avoid currencies in our model for these reasons.

Jostova et al. (2012) show that momentum does not work with investment grade bonds, but works very well with credit-sensitive or non-investment grade bonds over the period 1973-2010. The premiums for non-investment grade – or high yield bonds are nearly 200 basis points per month.

Moskowitz and Grinblatt (1999) show that industry momentum accounts for nearly all of the individual stock momentum profits. In other words one could have captured the cross-sectional US equity momentum effect by investing in the best industries in aggregate and shorting the worst industries. This finding supports the use of industry or sector ETFs as a viable approach to capturing stock momentum. Chan, Hameed and Tong (2000) show that cross-sectional momentum exists across different country markets. This supports the use of country ETFs as an alternative approach to complement sector or industry momentum strategies. As a result, for simplicity we prefer to use broad country, sector, or style ETFs to capture the momentum effect within the equity asset class category.

Momentum Across Asset Classes

Much of the research we have seen has demonstrated a strong and durable within asset class effect. This begs the obvious question as to whether momentum works at the asset class level such as choosing between stocks or bonds. This has strong implications for the favorability of a strategic or policy allocation approach versus a more dynamic or tactical approach that changes in response to market conditions. As we have shown, some of the best investment managers in the world have employed this approach, but academic studies on this effect are relatively new. Blitz and Van Vliet (2008) of the highly successful investment firm Robeco conducted the seminal research in this area. They used a universe of 12 different broad asset classes: US large-cap equities, US mid-cap equities, US real estate equities (REITS), UK equities, Japanese equities, emerging markets equities, US Treasuries, US investment grade bonds, and US high yield bonds, German bonds, Japanese bonds, and US 1-month LIBOR cash which was a proxy for the risk-free alternative. They showed that over the 1986-2007 period, a cross-sectional momentum strategy using past asset class returns holding the top quartile of assets and shorting the worst quartile would have generated nearly 8% annually. Furthermore the returns were highly consistent over time. Blitz and Vliet also show that the cross-asset class momentum was highly correlated with Fama’s popular momentum factor – which is difficult to capture in real life unless you are willing to go long and short hundreds of individual stocks. They suggest that using asset classes is far more practical, and they further demonstrate that an asset class momentum strategy is easily profitable after accounting for realistic transaction cost assumptions.

Blitz and Vliet also interpret the results with a similar hypothesis that we proposed earlier; markets are perhaps highly macro-inefficient. Samuelson – who originally made this assertion – believed that the market was more likely to be micro-efficient (i.e. momentum across individual stocks would be less likely to work) than macro-efficient due to the relative supply of arbitrage capital (money available to correct mispricing). Blitz and Vliet theorized that there are fewer sources of arbitrage capital to eliminate macro-inefficiencies since most of the asset allocation decisions are either highly regulated or outsourced to fiduciary agents such as pension plans. In contrast, most of the active management world has the ability to use cross-sectional momentum within their own asset class. For example a domestic equity mutual fund manager can use momentum to pick stocks. This implies that the half-life or longevity of excess profitability for momentum strategies using individual stocks should be much shorter than for asset classes. Howerver, momentum strategies across broad market categories within an asset class.It is more difficult for a Large Cap equity manager to dynamically over/underweight the best performance category (such as Large Value or Small Growth) than it is for them to overweight individual stocks based on momentum since they are penalized for style drift. Blitz and Van Vliet also show that only a small minority of hedge funds employ such cross-asset momentum approaches. Therefore the competition or supply of arbitrage capital for across asset momentum strategies (which would drive their own demise) is very low. This implies that a dynamic approach across asset classes should be very durable over time in terms of profitability – more durable than applying it to individual stocks.

Butler, Philbrick, Gordillo and Varadi (2013) in “Adaptive Asset Allocation: A Primer” take an advanced approach to applying cross-sectional momentum across asset classes. They show that a strategic asset allocation is rarely favorable and often produces a significant imbalance of risk in times of crisis. They suggest that investors should employ a cross-sectional momentum approach to adapt to changes across global markets and different economic regimes. Butler et al use a diverse set of broad asset classes for their analysis during the period between 1995 and 2012. The best performing assets show a higher probability of rising the next month relative to the worst-performing asset classes. The chart below summarizes these findings:

Butler et al. also show that combining a cross-sectional asset class momentum approach with risk optimization (incorporating volatility and correlations at the individual asset and portfolio level) produces far superior risk-adjusted results. An “adaptive” approach that changes portfolio allocations using asset class momentum, volatility and correlations (or any of the above inputs) is suggested to be superior to a strategic or policy allocation – especially for investors that must plan for withdrawing funds in retirement. Using a cross-sectional momentum approach in isolation to select asset classes in an adaptive portfolio nearly doubles the safe withdrawal rate – the return that an investor can safely withdraw from their portfolio without running out of money – versus using a passive strategic approach of holding assets in an equal weight allocation. An adaptive approach that incorporates risk optimization produces even better results. The conclusion is that an adaptive or dynamic asset allocation approach using momentum can improve both investment performance as well as the probability of successful financial planning outcomes.

Hammerich (2012) also demonstrates evidence of multi-asset cross-sectional momentum. Using a conventional momentum methodology, and a 12-year sample period with 50 different indices, he finds that going long the best assets and shorting the worst assets earned significant excess returns of 9.19 percent annually. Hammerich also found that positive risk asset performance from equities and commodities as well as low volatility (low VIX) were factors that tended to accelerate the performance of across asset class momentum. Bull markets tended to accelerate across asset class momentum and bear markets tended to erode across asset class momentum. Again we see more evidence that the “macro” environment is important for engaging in cross-sectional momentum strategies regardless of whether one is using individual stocks or broad asset classes.

In summary, the research shows conclusively that cross-sectional momentum can be applied both within and across asset classes. These findings are universal and have worked since the beginning of organized markets and have demonstrated stability across a wide range of economic regimes and survived major world events. Research shows that while within asset class cross-sectional momentum is still strong, it has perhaps less durability than across asset classes. Clearly both approaches are important sources of value and can be easily layered on top of one another to generate additional value. This is one of the cornerstone concepts of our Dynamic Asset Allocation model.

Time Series Momentum

Academic studies supporting time series momentum are relatively new, however hedge funds and commodity trading advisors (CTAs) that call themselves “trend-followers” have made use of this concept successfully in the futures markets for over 50 years. Some of the famous money managers that employ this approach are John Henry, Ed Seykota, Richard Dennis, William Eckhardt, and David Winton. Many of the most successful CTA/hedge funds have employed this style and are often referred to as “systematic investors” for their rules-based quantitative approach. Hedge fund giant AQR was highly successful using cross-sectional momentum strategies (and also combining value and momentum together), but only recently began to publish research and utilize what they refer to as “time series momentum.”

As previously mentioned, time series momentum is the tendency of the sign of past returns for a given asset to predict the sign of future returns. A typical time series momentum strategy would entail going long an asset if the 12-month return minus the T-bill rate is positive, and short if the return is negative. Trend-following compares the price to a moving average of price to determine whether to go long or short , but the research shows that the signals generated by trend-following and time series momentum are often highly correlated and capture the same effect. More recently, Gray (2015) of Alpha Architect does a review of modern asset allocation methods. He shows that combining both time series momentum and trend-following signals is an improvement over either method in isolation. This method is termed “Robust Asset Allocation” (RAA) since it produces superior risk-adjusted performance to using only time series momentum in isolation.

Moskowitz, Ooi (from AQR) and Pedersen (2012) investigate ‘‘time series momentum’’ in 58 different futures markets; equity indices, currencies, commodities, and bonds for the period between 1965 and 2009. They playfully title their findings “A Trending Walk Down Wall Street” – to poke fun at passive investing giant Burton Malkiel’s famous book “A Random Walk Down Wall Street.” Moskowitz et al. find that time series momentum works for every single one of the 58 different markets considered. The chart below shows the risk-adjusted return (gross Sharpe ratio) for all 58 markets. What is most interesting is that time series momentum has both high and consistent performance across traditional equity and fixed income markets that form the core of investor’s portfolios.

To further support the robustness of this approach, Greyserman and Kaminski’s demonstrate an incredible 800 year backtest of Time Series Momentum in their book: Trend Following with Managed Futures: The Search for Crisis Alpha. This time frame is much longer than the studies used to support the premise of earning returns through a “buy and hold” investing approach. If one believes in buy and hold based on the limited evidence that was available spanning the last 200 years, then clearly it is equally if not more reasonable to expect that a trend-following approach is likely to be a profitable strategy over time. The authors included 84 markets; equities, fixed income, commodities, and currencies as they became available starting in the year 1200 through 2013. They used 12-month returns to generate the signal – long if returns were positive, short if returns were negative. All positions were sized equally using volatility to normalize bets across markets. The annual return of this strategy was 13% with an annual volatility of 11% and a Sharpe ratio of 1.16.

representative trend following portfolio from 1200 to 2013

Trend Following with Managed Futures

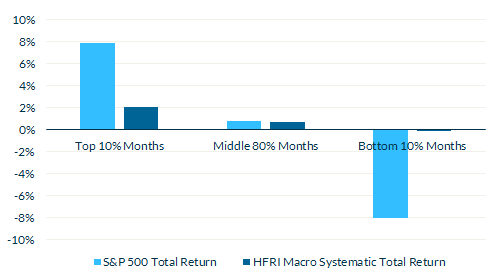

A diversified portfolio of time series momentum (or trend-following) applied to all asset classes demonstrates substantial abnormal returns but more importantly, it performs best during extreme markets. The graphic below shows how time series momentum performed over an even longer backtest (courtesy of AQR) versus a traditional 60/40 portfolio of stocks and bonds during different crisis events (Figure 16).

During almost all of the major crisis events a time series momentum strategy would have produced positive returns while a traditional strategic approach would have lost money. This is not just empirical evidence, since trend-following hedge funds (often called “Macro Systematic”) have demonstrated strong crisis performance using such strategies in real time:

The results show that trend-follower performance has indeed demonstrated protection during the worst months for the equity markets. However, it also shows that a diversified trend-following strategy has under-performed during the best months. This is because a trend-following or time series momentum strategy typically trades dozens of different markets both long and short with an absolute return mandate and does not attempt to harvest equity returns specifically. However, as we previously illustrated, the distribution of returns for a dynamic strategy is likely to have lower volatility – that means smaller gains and smaller losses – and as a consequence part of the upside during the best market conditions is sacrificed to reduce losses during the worst market conditions.

Time Series Momentum on Asset Classes

From a practical perspective, most advisors and investors do not have access to many of the exotic markets available to a CTA or hedge fund. Furthermore, they are constrained from being able to go short and must construct a suitable long-term portfolio including mostly conventional asset classes such as stocks and bonds. Since time series momentum shows strong evidence of being able to forecast the sign of returns, this does not pose much of a problem. In fact, it could be argued that using time series momentum on asset classes from the long side only is a superior approach because one is expected to earn a long-term return just from buying and holding the same assets. If we imagined flipping a coin where if heads landed we went long and tails landed we went short – the expected return to such a random strategy would be zero. However, if we flipped coins and if it landed on heads we went long stocks, and if it landed tails we held cash, the expected return would be 50% of the long-term equity return plus 50% of the cash rate. Since time series momentum is far superior to a coin flip and is often able to identify periods of negative returns, it is possible to achieve greater that 100% of the long-term equity return.

In the chart below using time series momentum from the long side only on equities shows exceptional absolute and crisis performance:

The time series momentum strategy would have actually outperformed the S&P500 and held cash positions most of the time during the bear markets. A reputable Wharton professor Jeremy Siegel presented further evidence in his book – “Stocks for the Long Run (2002) – that showed a trend-following approach would have worked on the Dow Jones Industrial Average (DJIA) going back as far as 1900. Siegel found that this approach would have generated superior returns and risk-adjusted returns versus just buying and holding the index. Ironically, Siegel’s book is often cited by passive investors to justify a buy and hold approach. Siegel’s finding with regard to trend-following is important because we cannot always rely on the long-term return to stocks or other asset classes such as bonds. The trend-following strategy would have captured most but not all of the gains in up markets, but reduced risk and occasionally earned positive returns in down markets. Sometimes playing defense is the only option for investors to preserve capital. Perhaps the primary fear that both investors (and the Fed) have is that we will have a Japan-style deflation and poor equity market returns. For buy and hold (buy and hope?) investors with a passive approach this scenario is disastrous to their returns. However, applying time series momentum can help reduce the risk of this scenario substantially:

The buy and hold investor would have lost more than 20% over a 10-year period while a time series momentum investor would have actually made a positive return of over 15%.

Faber (2006) in his landmark paper: “A Quantitative Approach to Tactical Asset Allocation” investigated the premise of holding a diversified portfolio of asset classes using a trend-following approach which is similar to time series momentum. Faber’s test used the price in relation to the 10-month moving average of price to generate buy and sell signals. The assets investigated were extended using publicly traded indices including the Standard and Poor’s 500 Index (S&P 500), Morgan Stanley Capital International Developed Markets Index (MSCI EAFE), Goldman Sachs Commodity Index (GSCI), National Association of Real Estate Investment Trusts Index (NAREIT), and United States Government 10-Year Treasury Bonds. If the trading signal indicated that the market was going down (price < moving average), then the proceeds were invested in treasury bills. The results from 1972 – 2005 showed that for each asset, using a trend-following approach reduced risk and maximum drawdown, and in most cases increased returns above buy and hold. A diversified portfolio that employed the trend-following approach would have generated equity-like returns with bond-like volatility and drawdown, and over thirty consecutive years of positive returns. Faber further shows that employing this type of model is practical even accounting for transaction costs and taxes since portfolio turnover tends to be low and most of the gains tend to be long-term. A recent update of the study shows the “out-of-sample” performance of the exact same strategy on the same asset classes through the financial crisis versus an equal weighted buy and hold portfolio of the same assets:

Clearly applying a time series momentum or trend-following approach to asset classes can substantially reduce risk versus a policy or strategic portfolio, and potentially enhance returns as well.

Combining Time Series and Cross-Sectional Momentum

The natural question is whether combining time series momentum with traditional cross-sectional momentum will yield superior results than either in isolation. Common sense dictates that it should be an improvement to use both because they are a) not perfectly correlated (see Moskowitz et al.); b) traditional cross-sectional momentum strategies tend to suffer in down markets – especially if one is not constructing a long/short market neutral portfolio. Antonacci (2012) in his paper: “Risk Premia Harvesting through Dual Momentum” tests the combination of cross-sectional and time series momentum with different asset class categories such as Equities, Real Estate, Credit and Economic Stress (Treasuries and Gold) over the period from 1974 to 2011. He shows that this approach yields higher returns and risk adjusted returns than any of the assets in their respective categories with much lower maximum drawdowns. Furthermore, combining both types of momentum was superior to using either in isolation across each asset class category. He concludes that combining time series momentum (he calls this “absolute momentum”) with cross-sectional momentum (the combination being Dual Momentum) yields superior returns and risk-adjusted returns than either in isolation. We use both time series and cross-sectional momentum in our models to enhance returns and reduce risk.

Conclusion

Investors as always face an uncertain future. Their financial goals can be jeopardized by unexpected changes in global market returns. A portfolio management approach that can constantly adapt to changes in financial markets over time is a necessity. The typical approach is to use investment committees where experts analyze global market trends and adjust their portfolios accordingly. However, research has shown that expert decision making across various fields including portfolio management has a poor track record, and tends to underperform simple quantitative rules that extrapolate from the past.

Employing the use of momentum or trend-following is the simplest and most effective way to adapt to changes in financial markets. Research shows the best approach historically has been to observe the pattern of past behavior for asset classes to determine both the expected relative performance and sign of expected returns. This is captured in a dynamic approach to asset allocation that uses different types of momentum to form portfolios.

Even the greatest skeptics from the camp of passive investors acknowledge that momentum is a legitimate anomaly. The academic research supporting the use of momentum spans the history of organized markets. Most importantly, some of the greatest investment managers of all time have used this approach predominantly to achieve their returns. We believe a Dynamic Asset Allocation approach that uses various forms of momentum is the optimal solution for portfolio management. The application of a dynamic asset allocation approach can potentially improve both investment returns and increase the probability of achieving financial planning outcomes.

References

- “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency,” 1993, Jeegadeesh and Titman, The Journal of Finance

- “The Behavior of Stock Market Prices,” along with his article “Efficient Capital Markets: A Review of Theory and Empirical Work,”1970, Eugene Fama, The Journal of Finance

- “Common risk factors in the returns on stocks and bonds,” 1993, Eugene Fama and Kenneth French, Journal of Financial Economics

- Dimensional Fund Advisors (DFA), http://www.dimensional.com/

- AQR, https://www.aqr.com/

- Turtle Trader – John Henry http://turtletrader.com/trader-henry/

- “Cliff Asness: A Hedge Fund Genius Goes Retail,” 2011, Fortune

- “Variables that Explain Stock Returns.” Ph.D. Dissertation, 1994, Asness, C.S., University of Chicago

- “Size, Value, and momentum in international stock returns,” 2012, Eugene Fama, Kenneth French, Journal of Financial Economics

- “Do Industries Explain Momentum?” , 1999, Moskowitz, T.J., Grinblatt, M. Journal of Finance

- “Efficient Market? Baloney, Says Famed Value And Momentum Strategist Cliff Asness,” 2014, Forbes Magazine

- “Momentum Strategies.” 1996, Chan, Louis K.C., Narasimhan Jegadeesh, and Josef Lakonishok, Journal of Finance

- “International Momentum Strategies.” 1998, Rouwenhorst, K.G,. Journal of Finance

- “Dissecting Anomalies.” 2008, Fama, E.F. and French, K.R., Journal of Finance

- “Understanding the Nature of the Risks and the Source of the Rewards to Momentum Investing.” 2001, Grundy, B. F. and Martin, S.R. Review of Financial Studies

- “A unified theory of underreaction, momentum trading, and overreaction in asset markets.” 1999, Hong, H., Stein, J.C. Journal of Finance

- “A Model of Investor Sentiment.” 1998, Barberis, N., Shleifer, A., Vishny, R. Journal of Financial Economics

- “New facts in finance Cochrane,” 1999, John H., NBER working paper # 7169.

- “On the predictability of stock returns in real time.” 2001, Cooper, Michael, Roberto Gutierrez Jr., and Bill Marcum, Journal of Business

- “Is time series based predictability evident in real time?” 2002, Cooper, Michael and Huseyin Gulen, Working paper. Purdue University.

- Stock return predictability: A Bayesian model selection perspective.” 2002,Cremers, Martijn, SSRN

- An Intertemporal Capital Asset Pricing Model, “ 1973, Robert C. Merton, Econometrica, Review of Financial Studies

- Asset Allocation vs Security Selection: Their Relative Importance,” 2011, Staub and Singer, CFA Publications

- Expert Political Judgment: How Good Is It? How Can We Know?” 2005, Phillip Tetlock

- 212 Years of Price Momentum (The World’s Longest Backtest: 1801-2012),” 2013, Christopher Gezcy and Mikhail Samonov, SSRN

- Fact,Fiction and Momentum Investing,” 2014, Cliff Asness, Andrea Frazzini, Ronen Israel, and Tobias J. Moskowitz, SSRN

- Momentum Strategies in Commodity Futures Markets,” 2007, Joelle Miffre and Georgios Rallis, SSRN

- “REIT Momentum and the Performance of Real Estate Mutual Funds,” 2008, Jeroen Derwall, Joop Huij, Dirk Brounen, Wessel Marquering, SSRN

- “Currency Momentum Strategies,”2011, Lukas Menkhoff, Lucio Sarno, Maik Schmeling, Andreas Schrimpf, SSRN

- “Momentum in Corporate Bond Returns,” 2012, Gergana Jostova, Stanislava Nikolova, Alexander Phillipov, Christof W. Stahel, SSRN

- “Profitability of Momentum Strategies in the International Equity Markets,” 2000, Kalok Chan, Allaudeen Hameed and Wilson H.S. Tong, Journal of Financial and Quantitative Analysis

- “Global Tactical Cross-Asset Allocation: Applying Value and Momentum Across Asset Classes,” 2008,Blitz and Van Vliet, The Journal of Portfolio Management

- “Adaptive Asset Allocation,” Adam Butler, 2012, Mike Philbrick, Rodrigo Gordillo, David Varadi, SSRN

- “Momentum Investing: The Multi-Asset Evidence,” 2012, Casper Hammerich

- “Robust Asset Allocation,” 2015, Wesley Gray, Alpha Architect, http://www.alphaarchitect.com/blog/2014/12/02/our-robust-asset-allocation-raa-solution/#.VP4wiPnF_O4

- “Trend Following with Managed Futures, The Search for Crisis Alpha,” 2014, Alex Greyserman and Kathryn M. Kaminski, Wiley

- “The Strategic View; The Strategic Case for Momentum,” 2012, Jonathan Smith, http://www.schroders.com/globalassets/schroders/sites/pensions/pdfs/120504-strategicview-caseformomentum.pdf

- “A Quantitative Approach to Tactical Asset Allocation,” 2006, Mebane Faber, SSRN

- “Risk Premia Harvesting through Dual Momentum ,”2012, Gary Antonacci, SSRN

- “An Intertemporal Capital Asset Pricing Model”, 1973, Robert C. Merton, Econometrica

- “The Quants”, 2010, Scott Patterson, Crown Publishing

- “Active Share and Mutual Fund Performance”, 2013, Antti Petajisto,SSRN

- “Dynamic Asset Allocation”, 2010, James Picerno, Bloomberg Press

- “Portfolio Theory and Capital Markets”, 2000, William Sharpe

- “Investing for the Long Run when Returns are Predictable”, 2000, Nicholas Barberis, Journal of Finance

- “The Theory of Speculation”, 1900, Louis Bachelier – translated in 2006 Princeton University Press

- “Samuelson’s Dictum and the Stock Market”, 2005, Jee Jung and Robert Shiller, Economic Inquiry

- “Portfolio Selection”, 1952, Markowitz, Journal of Finance

- “Multifactor Explanations of Asset Pricing Anomalies”, 1996, Eugene Fama and Kenneth French, Journal of Finance

- Kenneth French Data Library: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

- “Style Rotation and Momentum and Multifactor Analysis”, 2003, Kevin Wang, Working Paper

- “Tactical Alpha: The Case for Active Asset Allocation”, 2013, Adam Butler, GestaltU

- “Time Series Momentum”, 2012, Tobias Moskowitz, Yao Ooi, Lasse Pedersen,Journal of Financial Economics

- “Irrational Exuberance” 3rd Edition, 2015, Robert Shiller, http://irrationalexuberance.com/main.html?src=%2F

- “Stocks for the Long Run”, 5th Edition, 2014, Jeremy Siegel

- “Asset Allocation vs. Security Selection; Their Relative Importance”, Renato Staub and Brian Singer, CFA Institute 2011

- “The Case for Dynamic Asset Allocation”, 2012, BNY Mellon Asset Management/Mellon Capital

- “A Non-Random Walk Down Wall Street”, 1999, Lo and MacKinlay, Princeton University Press

- “The Winner’s Curse: Paradoxes and Anomalies of Economic Life”, 1992, Thaler, Princeton University Press

Endnotes

-

- Asset class data sourced from Morningstar, source names for each asset as follows:

- In Figure 3 the formation period for momentum used the average of 5 different lookbacks – 1, 3, 6, 9, and 12 months – to compute a composite compound annual return (CAGR). This composite CAGR was used to rank asset classes for selection each month starting in January of 1987 and finishing at the end of January in 2015. In every month the top (or bottom) % of assets were chosen based on the formation period composite performance and subsequently held until then next month. This “out of sample” data was aggregated to form an equity curve for the purposes of computing performance and risk metrics. The fifteen asset classes used in Figure 3 were taken from the database in endnote 1: 1) S&P500 2) Bonds 3) Commodities 4) Real Estate 5) International 6) T-Bill 7) High Yield 8) Growth 9) Value 10) Small Cap 11)Emerging 12)Corp. Bonds 13) Gold 14) Treasury 15) Mid Cap.

- In Figure 4 the formation period for time series momentum used the average of 5 different lookbacks – 1, 3, 6, 9, and 12 months – to compute a composite compound annual return (CAGR). This composite lookback was used to determine whether the return was positive or negative for each individual asset for each month starting in January of 1987 and finishing at the end of January in 2015. All assets were tested individually rather than as a portfolio. If the composite performance of a given asset based on the formation period was positive a long position was held in that asset. If the composite performance was negative, a position in T-bills was held instead of holding the asset. Positions generated on the basis of this composite performance indicator were subsequently held until then next month. This “out of sample” data was aggregated to form an equity curve for the purposes of computing performance and risk metrics. The fourteen asset classes used in Figure 4 were taken from the database in endnote 1: 1) S&P500 2) Bonds 3) Commodities 4) Real Estate 5) International 6) High Yield 7) Growth 8) Value 9) Small Cap 10)Emerging 11)Corp. Bonds 12) Gold 13) Treasury 14) Mid Cap.

- Asset class data sourced from Morningstar, source names for each asset as follows:

Important Information

This paper is copyrighted by Blue Sky Asset Management, LLC (“BSAM”) with all rights reserved. Any reprinted material is done with permission of the owner. This material has been prepared for informational purposes only and is not an offer to buy or sell any security, product or other financial instrument. Past performance is not necessarily a guide to future performance. All investments and strategies have risk, including loss of principal.

BSAM and its affiliates do not render advice on tax and tax accounting matters to clients. This material was not intended or written to be used, and cannot be used or relied upon by any recipient, for any purpose, including the purpose of avoiding penalties that may be imposed on the taxpayer under U.S. federal tax laws.

The author(s) principally responsible for the preparation of this material are expressing their own opinions and viewpoints, which are subject to change without notice and may differ from the view or opinions of others at BSAM or its affiliates. Any conclusions presented are speculative and are not intended to predict the future of any specific investment strategy. This material is based on publicly available data as of the publication date and largely dependent on third party research and information which we do not independently verify. We make no representation or warranty with respect to the accuracy or completeness of this material. One cannot use any graphs or charts, by themselves, to make an informed investment decision. Estimates of future performance are based on assumptions that may not be realized and actual events may differ from events assumed. BSAM is not acting as a fiduciary in presenting this material. Benchmark indices are presented for illustrative purposes only and do not account for deduction of fees and expenses incurred by investors.

The strategies discussed in this material may not be suitable for all investors. We urge you to talk with your investment adviser prior to making any investment decisions.